Donate

In order to provide a range of incredibly diverse experiences at the LCCC, we depend on donors like you. There are many ways that you can help support our mission and ensure that we can continue to offer hundreds of creative opportunities each year for people of all ages and income levels.

Ways to Give

Become a Member

To offer a wide array of enriching experiences at the LCCC, we rely on generous donors like yourself. By becoming a member, you're not only aiding our cause but also guaranteeing the ongoing provision of numerous creative avenues annually, accessible to individuals of all ages and financial backgrounds. Members can enjoy event discounts, exclusive access to member-only gatherings, and more. Our community of members is actively shaping tomorrow, all the while relishing the current joys. Come be a part of it!

Annual Campaign

You can make an even bigger impact on the lives of your friends, your family and your neighbors in Lincoln City, by supporting the Annual Campaign. The funds raised in the Annual Campaign go toward everyday operating expenses like paper towels, utility bills and routine maintenance—key support for a public facility that hosts activity nearly every day of the year. Give by Dec. 31, and make a difference.

Sponsorships

Are you a cheerleader for children’s art? A thespian through and through? Over the moon for opera? You can express your feelings (and help others catch the spirit, too) by sponsoring your favorite thing at the Cultural Center! We are looking for arts-minded individuals and businesses for upcoming programs and opportunities.

To learn more, contact Niki Price at 541-994-9994 or lcccdirector@gmail.com.

Lincoln City Endowment Fund

We are launching the Lincoln City Endowment Fund - a long-term investment in our mission and the cultural vitality of our region. This fund will generate steady, sustainable income for generations to come, ensuring that art, music, education, and community engagement continue to thrive on the Oregon coast, no matter what challenges lie ahead.

What's the goal? We're asking you to join us at the ground level. Our initial goal is to raise $25,000 by October 2025 to launch the fund with the Oregon Community Foundation.

Join the Legacy Club:

Donors who contribute $1,000 or more to the Endowment Fund will join The Legacy Club, a special group of members who will be recognized on a permanent Donor Recognition Wall installed at the Cultural Center's west entrance.

Donate any amount to the Endowment Fund in four simple ways:

- If you are 70 1⁄2 or older, you can reduce your tax bill by donating to the Endowment Fund directly from your Individual Retirement Account. Meet your required minimum without paying taxes on the distribution, up to $100,000 a year.

- Designate our organization as the beneficiary of your life insurance or retirement account.

- Make a bequest in your will.

- Make a donation by cash, check or credit card.

Plaza Commemorative Brick Program

The Lincoln City Cultural Plaza is now complete, offering a beautiful and welcoming space where art, culture, and community converge. This transformation was made possible by the generosity of those who believe in the power of arts and culture. Now, you can be a part of this legacy by purchasing a brick - an enduring tribute to your support for the arts.

With a tax-deductible gift of $300 for an 8'' x 8'' brick or $150 for a 4'' x 8'' brick, you can have a personalized message engraved and permanently placed in the Cultural Plaza. Your donation will help ensure the Cultural Center remains a vibrant hub for arts and culture for generations to come.

Fred Meyer Community Rewards

Fred Meyer is donating $2.6 million each year—up to $650,000 each quarter—to the local schools, community organizations and nonprofits of your choice. All you have to do is link your Rewards Card to LCCC and scan it every time you shop at Fred Meyer.

Are you a Fred Meyer Customer?

You are now able to link your Rewards Card to Lincoln City Cultural Center. Enroll as account 91331 or look up Lincoln City Cultural Center. Whenever you use your Rewards Card when shopping at Freddy’s, you will be helping us earn a donation from Fred Meyer. If you do not have a Rewards Card, you can sign up for one at the Customer Service Desk of any Fred Meyer store.

Fred Meyer is donating $2.6 million each year—up to $650,000 each quarter—to the local schools, community organizations and nonprofits of your choice. All you have to do is link your Rewards Card to LCCC and scan it every time you shop at Fred Meyer.

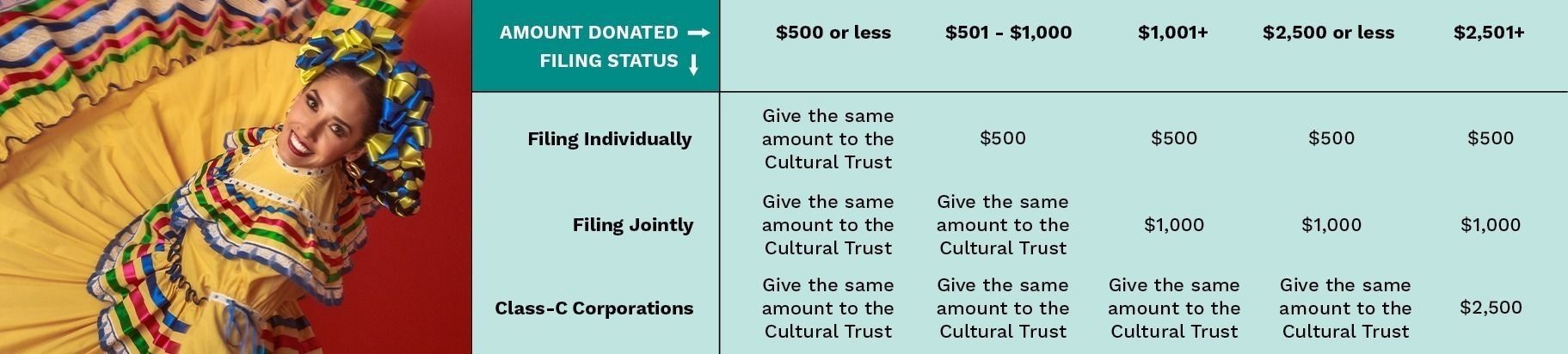

Tax Credit from the Oregon Cultural Trust

If you donated to any arts, heritage or humanities nonprofits in Oregon this year, you are eligible to direct a greater portion of your taxes—taxes you’re going to pay anyway— to supporting cultural projects in the state with the Cultural Tax Credit.

If you think Oregon should provide more funding for arts, heritage and humanities projects, here’s how to do your part:

- Total what you gave to the nonprofits on this list during the calendar year.

- Give to the Cultural Trust online or by mail by December 31. Wondering how much to give? See our recommendations below.

- On your State Tax Form, report your donation to the Oregon Cultural Trust. You’ll get 100% of it back!*

To learn more, visit culturaltrust.org, or contact Niki Price at 541-994-9994 or lcccdirector@gmail.com.

* Up to $500 for individuals, $1,000 for couples filing jointly, and $2,500 for class C-corporations.

IRA RMD Contribution

Required Minimum Distribution charitable tax break (QCD) is permanent

If you're required to take a minimum distribution (RMD) from your IRA starting at age 70½, you have the option to make that distribution tax free from Federal or Oregon taxes by directing some of it to the charity of your choice as a Qualified Charitable Distrition (QCD).

In understanding qualified distributions, it's helpful to recall the basics of required minimum distributions (RMDs): If you're age 70½ or older, you generally must withdraw a minimum amount each year from your traditional IRAs. The money you're required to withdraw gets added to your taxable income. Failure to take your RMD by year-end could result in a stiff IRS penalty—50% of the amount you should have withdrawn.

Under the QCD rule, beginning at age 70½, you can have all or part of your distribution made directly from your IRA to a qualified charity (up to $100,000 per taxpayer, per year). Unlike conventional RMDs, QCDs aren't subject to ordinary federal or state income taxes. You can give your RMD to charity anytime during the year now that the tax break is permanent.

You need to transfer the money directly from the IRA to the charity for it to count as the tax-free transfer. Ask your IRA administrator and the charity about making a direct transfer, or you can have the IRA administrator send a check from your account to the charity. If you have check-writing privileges for your IRA, you can write a check to the charity. Give us a heads-up, so we know the contribution came from you and can send you an acknowledgement.

For example, suppose that in 2015 you're over age 70½ and you'd like to make a contribution to your favorite charitable organization. You may have your RMD made payable directly to the Lincoln City Cultural Center, and then designate it as a qualified charitable distribution on your tax return. You'll have satisfied that amount of your distribution requirement, and you won't have to pay income taxes on that money. Be sure to take those QCDs to your tax preparer to be sure it is recorded properly on your returns so that counts toward meeting your RMD for the year but is not counted as income.

Be aware that you can't also claim the qualified distribution as a charitable tax deduction—the amount is simply excluded from your taxable income.

So which is better: the tax-free transfer or the charitable deduction?

If you make a tax-free transfer from your IRA to charity, you can’t also deduct that money as a charitable contribution. But the tax-free transfer could give you extra benefits. You don’t need to itemize your deductions to get a tax benefit from the gift (and many people who no longer have a mortgage don’t itemize their deductions). Making the tax-free transfer also keeps the money out of your adjusted gross income. That could help you avoid the Medicare high-income surcharge, which boosts your Part B and Part D premiums if your AGI is more than $85,000 if single or $170,000 if married filing jointly. Keeping the money out of your AGI could also make less of your Social Security .benefits taxable

Check with your own tax advisor about the impact on your personal tax situation.